First and foremost you’re in a Debt-Based Economy system.

If you don’t know what that means…Google it.

If you know, then you ought to know you’re a borrower if you’ve ever

used (paper) money sometime in your life, even if you have none right

now in your wallets or pockets, or have never made any personal loans

from the bank.

“But, but… I work and I’m earning my money?”

Secundo:

Haven’t you heard of Fractional Reserve Banking?

So-called money in circulation is created by debt and is an IOU.

If you don’t know that…Google it.

You work to pay your own debts including all those created in the system, or by your government.

This’ no rocket 🚀 science. Its plain, simple and clear.

All it takes to gulp this down your throat and digest it, is a simple act of research and observation.

One borrows (thus a borrower) because one have none.

Contrary to popular beLIEfs, your pockets are empty, actually.

You don’t need a slide rule, a set of log tables or a high frequency trading algorithm to see the light. Everyone on Main Street now knows that the Western banking cartel’s fixation with debt colonisation is a busted flush. Debt does not work as the basis of a global financial system.

Behind the scenes, all the indications are that universal debt forgiveness is set to be announced. A global debt jubilee is waiting in the wings. The Doctrine of Odious Debts has been spectacularly revisited. The default position of the global financial system is to be permanently reset. The vaults are stocked. The precious metals are audited. The new gold-backed regional currencies are printed, minted and ready.

The most recent catalyst for change has been Iraq. Before the Western cabal’s US-UK war of occupation and plunder began in Iraq in March 2003, Iraqi exiles expressed the hope that in a post-Saddam democratic Iraq, there would be a fair and equitable disposition of Saddam’s debts.

These Iraqis wanted the future administration of Iraq and the international community to review the debts accumulated under Saddam’s régime. Those loans which had been used for benign purposes should be restructured and paid back by Iraq over a prudent time period. Those loans which were used for objectionable purposes and which did nothing to enhance the well-being or prosperity of the Iraqi population at large, should be struck off the record immediately and completely.

This illustrates one of the core principles of debt forgiveness. Why should Iraqis be forced to repay the US, the British, the French, the Germans, the Russians, and all the others who had financially supported Saddam’s oppression of them?

The Iraqi argument for debt forgiveness had a sound basis in law. It reflects the century-old legal principle of the Doctrine of Odious Debts.

The Doctrine of Odious Debts was created to further international finance by limiting the ability of governments to repudiate debts. Three conditions had to apply before a sovereign state could repudiate a debt:

(1) The debt must have been incurred without the informed consent of the citizenry of the state.

(2) The debt must not have benefitted the citizenry of the state.

(3) The lender must have been aware of conditions (1) and (2) at the time that the loan papers were signed.

The United States employed these principles after the Spanish-American War to repudiate the Cuban debts.

If a despotic power incurs a debt which is manifestly not for the needs of the State, or not in the plain interest of the State, but is a debt incurred solely to strengthen the position of the despotic cabal as a self-serving faction within that State, the debt is odious. The debt is not an obligation for the nation; it is a cabal debt, a personal debt of the cabal which incurred it. And the debt falls with the fall of the cabal.

The Doctrine of Odious Debts not only promotes accountability, it promotes democracy in the debtor state as, one by one, the nature of the inherited debts are articulated in a public legislature.

The Doctrine of Odious Debts also promotes democracy in creditor states. In Canada and most European nations, the lending of state enterprises is generally hidden from taxpayers. Canada’s export credit agency, Export Development Canada, for example, is exempt from Canada’s Access to Information law.

In the case of Iraq, state agencies from France, Germany and Russia may have made questionable loans. Under an odious debt process, they would need to establish that they acted with due diligence to be entitled to repayment. Knowing this, they would be less likely to make questionable loans in the future.

Debt forgiveness and the Doctrine of Odious Debts also applies to individuals. The same principles have legal traction on loans or structured financial inducements made by financial institutions such as banks, mortgage lenders, insurance companies, stock-trading entities, energy conglomerates and pharmaceutical firms.

If the intention of the financial transaction tied to the loan, or tied to the financial inducement, is extortion, if it is, in effect, an élite scheme to bamboozle the borrower with small print or to blind him with science, that loan or inducement, should be struck off the record immediately and completely. The debt was not incurred with the informed consent of the borrower. The debt did not benefit the borrower. And the lender was well aware of these facts when the loan papers were signed.

More background about the concept of the Odious Debt can be found here (pdf – 11 pages – Jayachandran and Kremer) and, in the specific context of Greece in 2011, here. Murray Rothbard’s original 2004 piece on Repudiating the US National Debt can be found here. And The Center for Global Development’s 2010 review entitled: “Whatever Happened to the Jubilee? A 10th Anniversary Assessment of the Debt Relief Movement” is linked here.

Citing both Keen and Hudson, Yiamouyiannis is persuasive. When debt is fraudulent, debt forgiveness is both the logical and the only remedy for the situation. Whatever the name you give to the process – erasure, repudiation, abolishment, cancellation, jubilee – debt forgiveness will eventually have to emerge at the forefront of global efforts to solve the ongoing systemic financial crisis.

The only way to erase counterfeit money and counterfeit assets amounting to hundreds of trillions of dollars is to erase the debts associated with these fake assets. They are not toxic assets. They are fake assets.

Debt forgiveness accomplishes two important things. First, it eliminates the increasing and outsized portion of productive enterprise which is being employed to pay off unproductive obligations. Second, it clears the ground for new opportunities, new thinking, creative invention and positive entrepreneurialism.

Stentorian calls for austerity are nothing more than the delusional efforts of a fraudulent bankster status quo to avoid the consequences of its own error and fraud. The élite demands for austerity are a self-serving effort to kick the profit-can down the road in perpetuity. So bedazzled by the false wealth created by debt multiplication and its concomitant fantasy of ever-higher returns, the fraudulent bankster status quo continues to be stupidly amazed that ordinary people in the street are not spending money, and that the national economy is not picking up.

Productive human wealth has been trapped by establishment banksters in a web of parasitic theft, counterfeiting, liability evasion, non-regulation, and prosecutorial non-accountability. All the fundamental attributes of a functioning exchange economy have been warped to reward creative criminals.

Fabricated or parasitic so-called “wealth” destroys value by diluting the value of real productive wealth. Debt or credit which cannot be paid back is never an asset; it is always a liability. That some people in the market can be fooled into buying such liabilities and thus generate sale profits and transaction fees is risible.

The operating models upon which the modern debt nexus is historically based have no organic contact with reality. They assume unlimited growth and an unlimited ability to pay. When matched against the reality of real people paying ten times their salary for mortgages, which actually add more money owed to their principal (with negative amortization), require no money down, and set up balloon payments – large step-ups in payments after a few years – there is no possible way such people could not default within a predictable timespan.

Systemically, all debt which charges a percentage originates in delusion. Debt grows exponentially indefinitely; income and other growth cannot do this. This leads to a widening condition where the fruits of productive growth devoted to interest payments increase until those fruits are entirely consumed. Once this happens, stores of wealth (hard assets) begin to be cannibalised to make up the difference. You can see this now in Middle America where, absurdly, people are having to liquidate their retirement accounts to pay for their current cost of living.

The problem is compounded by a privately owned Federal Reserve syndicate which lends money into circulation at interest, and then allows the multiplication of this consumer debt-money liability through fractional reserve banking.

The total amount of money in circulation today can pay for only a tiny fraction of the total private and public debt. This fact alone is evidence of a kind of systemic fraud. This is why debt forgiveness makes not only moral, but also rational and mathematical sense. Finances require balancing to be coherent. There has to be some way to redress the systemic imbalance in Western macrofinance. There has to be some way to zero the scales in order to get an accurate weight of value, and to re-establish healthy value creation.

The problem with debt is that it creates scarcity. Scarcity stimulates fear. Fear drives manic competition. And manic competition favors opportunism, collusion, and concentrations of power. These élite concentrations of power translate into establishment abuse. The inevitable result is a visible collapse of legitimacy within the economic system. This is what is being seen now, all over the Western World, by Joe Public and his missus.

Debt forgiveness recognises the inherent, systemic, mathematical inability to make good on debts, and (or) the naked fact that the debt itself was manufactured through fraudulent means.

The foregoing twelve paragraphs précis some of the ideas which Zeus Yiamouyiannis has suggested in his writing on debt forgiveness. The best brief summary of his thoughts is probably here (01.09.11).

The situation is plain. You cannot solve the debt problem by issuing more debt. You solve the debt problem by cancelling, completely, all national, corporate and personal debt. You do this simultaneously across the planet, and you do it permanently. And then you recapitalise the whole bangshoot using an established resource base such as The World Global Settlement Funds and the associated US Dollar Refunding Project.

This next bit sounds exotic. But in future years it may well sound like a blinding glimpse of the obvious. You don’t establish the value of something by sticking it in a market. You establish the value of something by giving it away free and seeing what social value accrues as that something is used locally to energise cooperative livelihoods and free barter.

Interestingly, the core idea of global debt forgiveness is not restricted to the benevolent ivory towers of economic utopians. It is beginning to be talked about, in public, by national parliamentarians.

At the end of August 2011, in Ireland, the Irish Finance Minister, Michael Noonan, had to respond to organised calls for debt forgiveness in connection with his EuroZone nation’s struggling mortgage borrowers. The story was run prominently in the Business section of the Irish Times on Friday 2nd September 2011. Its headline was: “Minister rules out ‘free-for-all’ debt forgiveness. Noonan insists there is no magic bullet.” The article, by Simon Carswell and Colm Keena, can be found here.

What you may not know is that debt arose recently on the human stage. Throughout more than 99% of our history we have not even had a concept for debt. (The interested reader can pick up David Graeber’s excellent book Debt: The First 5000 Years for full story.)

Anthropological studies of hunter-gatherer societies reveal that there were no barter systems, no currencies to use for money, and — in the absence of these cultural artifacts — there was no debt. With all the great variation cross cultures one might expect from ethnographic research, the anthropologists found that some tribal communities engaged in “gift economies” where status arises from how generous a person is who has acquired wealth, while others have remained egalitarian and non-hierarchical for thousands of years by sharing their food and materials based on the principles of “from each as they are able, to each as they need.”

This belies the great misunderstanding about communism that treats it as a state-centric governing system, when in truth it is the foundational sentiment of any community that builds upon the trust and good will of social relations between people who know and depend upon one another — a condition that has held for all hunter-gatherer societies throughout our long 200,000 year history as a species.

Pick up an economics textbook at random and you will find a classic (and false) “just so” story about the need for barter systems to have money. They all go something like this: Steve has potatoes and needs some shoes. Bob has shoes but does not need any potatoes. They are unable to directly exchange goods due to this mismatch of need, and so must introduce a money system to preserve the value of currency across multiple exchanges that enable Steve to sell his potatoes to Sue and acquire money that he can then use to pay Bob for a pair of shoes. What this simple narrative conceals is the broad evidence from ancient cultures studied by anthropologists that no such problem arises in this way.

What really happens is that a warring society has arisen somewhere (to get a sense of how this happens, read my article about psychopaths and agrarian city states) and is in a mode of conquest. When this burgeoning empire conquers new land, the ruler imposes a system of taxation on the local populace to pay for the costs of war. This imposition of scarcity, by extracting resources from the local population to be hoarded by the warrior chieftain, is what leads to the emergence of barter systems and — in some instances — the introduction of a money system by the ruler.

In the absence of war and conquest, hunter-gatherer societies do not spontaneously create barter systems. Instead they share more or less equally within their tribe and only trade with other tribes through highly ritualized and often conflict-ridden exchanges that take place when two tribes come together for a brief interaction. The pathway that does lead to the emergence of barter systems takes place in agrarian societies where some kind of accounting system has been created to track debts. And from these accounting systems we do find that debt is present.

So where does debt come from if it isn’t naturally a part of human societies? Again it is the imposition of scarcity by the ruling class — designed to extract and hoard wealth in the hands of a powerful elite — that creates the notion of debt. Does this sound familiar in today’s context? Many countries were “modernized” throughout the 20th Century by introducing market systems that structure debt into the economies of newly founded nations. These nations now must pay tributes — in the form of interest payments — to external banks that extract wealth from the poor countries and hoard it in the coffers of wealthy countries.

Stated plainly, debt is created when a powerful group of people impose scarcity upon another group of people who have been conquered. This is the root cause of poverty. It is the destabilizing force of unequal societies that breeds civil unrest and revolution. Thus the need for Hebrew kings to introduce Jubilee. They knew that a revolution might cause the people to rise up and clear their own debts, while also uprooting the monarchy from power. In order to preserve their power base, they would routinely erase the debt and start again.

A Note About Debt and Moral Accounting

The astute reader may already be asking, “What does this story about the creation of debt say about the religious use of moral accounting?” You may have noticed that all the world religions have at their core a transactional relationship between God and humans — where each person owes a debt to their creator and must pay it either by relinquishing sin from their lives or by returning to their maker upon death.

This economic transaction frame for moral accounting is not present in all human societies. Those hunter-gatherer tribes practicing the ethic of distribution based on need have no concept for trading an eye-for-an-eye. Nor do they see a gift as something to be repaid, expressing disgust at the insult of treating their generosity in such a transactional manner.

Instead what anthropologists have found is that debt-based morality is only present in societies that already have accounting systems and also engage routinely in barter and monetary exchange. In other words, this moral accounting system is a product of war and conquest and not a natural part of human society. So the next time you feel a debt to one of your friends, society, or your maker it may help to keep this in mind.

What Would It Mean to Erase All Debt?

We are living in a time when too many of our financial resources are allocated to non-productive activities — principally the accumulation of wealth by “making money with money” and a myopic focus on economic activities that service our massive debts. This is why people work at jobs they hate. It is why investments are not being made in renewable energy, public education, the arts, health care, or the eradication of poverty. We have built a massive financial house of cards on debt — with money itself coming into being when loans are taken out, a pool that grows exponentially due to the interest that accompanies it — and so we are not able to bring consumer culture to an end or focus our creative talents on planetary sustainability.

By the way, this is exactly what my friends at /The Rules are trying to address in their global mobilization effort.

So if we were to erase all debt, the 7 billion people alive today could focus on their passions. We could all come together to address global threats — be they resource-based like the scarcity of fresh water or peaking of global oil production; or cultural like the loss of spiritual meaning in the secularization of society or the soullessness of employment drudgery that comes from working long hours at a mind-numbing job.

What comes to my mind is the way cities try to implement broad solutions to address economic development, transportation, resource management, social justice, and environmental concerns. They must operate within constrained budgets that keep draining further without a clear end in sight. I imagine what would be possible if everyone was able to set out on their own intellectual and experiential journeys without the fear of a debt-collector coming to their door. How then would the peoples of this world choose to live out their lives?

Perhaps you have your own dreams of a better world for you and your loved ones. What comes to mind for you? This is not merely an academic question, by the way, because we each participate in the social realities that are lent our beliefs, our actions, and our obligations. If we were to collectively decide that our debts are no more, they would cease to exist.

This is because what we take to be real in many respects becomes so as a self-fulfilling prophesy. We each have the power to be accountants — defining “the real” by choosing what to measure and imbuing it with significance. In this way, the Gross Domestic Product was claimed as an economic alter for measuring the progress of civilization in the 20th Century. Perhaps in the 21st we will replace it with Gross National Happiness or some other novel metric for capturing the essence of our values and purpose as a civilization on this Earth.

Watch the video below:

Joe Brewer is co-founder and research director of Culture2 Inc., a culture design lab for social good. He is a former fellow of the Rockridge Institute, a think tank founded by George Lakoff to analyze political discourse for the progressive movement.

I am no economist, far from it and thank god for that, but I have always opined that the Gross Domestic Product (GDP) is nothing more than the bank$ter$’ device deployed by their hired economists to con nations into debt slavery and rosily termed as the National Debt. That’s my take.

The GDP machine isn’t a real machine. Its levers, pedals, knobs, and buttons are largely imaginary fancies of arrogant imaginations.

The following passage is from page 239 of my late colleague Jim Buchanan‘s 1985 article “Political Economy and Social Philosophy” as it is reprinted in Moral Science and Moral Order, Vol. 17 of The Collected Works of James M. Buchanan:

“I list the engineering urge as one of three related strands of intellectual motivation that must be eliminated if political economy, and the work of its disciplinary practitioners, can assume an appropriate role in social philosophy…. [T]he engineers find their raison d’être in solving problems or, at one stage removed, in suggesting solutions to decision-makers faced with problems. It is in this sense that modern economists have sought pervasively to assume roles as putative problem solvers, as policy advocates, as advisers to governments, directly and indirectly.”

If and to the extent that – and for as long as – economists think of themselves as expert advisers to those who are in control of what are imagined to be the levers, pedals, knobs, and buttons of a machine called “the economy” – or of what Arnold Kling calls “the GDP factory” – they will regard those (today relatively few) economists of a free-market bent as hopelessly naive, unsophisticated, and worse than useless. Pointing out, as many market-oriented economists do, that the GDP machine isn’t a real machine, and that its levers, pedals, knobs, and buttons are largely imaginary fancies of arrogant imaginations, market-oriented economists invite the scorn of Engineering economists, the self-ordained doers of scientifically objective good who look upon straightforward explanations based upon supply-and-demand analysis and other basic economic concepts as simplistic efforts to obstruct the social-engineers’ quests to make earthly existence more heavenly.

Donald Boudreaux is a senior fellow with the F.A. Hayek Program for Advanced Study in Philosophy, Politics, and Economics at the Mercatus Center at George Mason University, a Mercatus Center Board Member, a professor of economics and former economics-department chair at George Mason University, and a former FEE president.

This is a continuation of last summer’s Jade Helm seven-state military exercise that many in the area saw as a prelude to military occupation. After Jade Helm came the US Army Special Operations Command’s Unconventional Warfare Exercise 16 (UWEX 16) that ran in Texas through June.

And now, after yet another police shooting in Charlotte, the city’s bus and light rail services ceased after midnight. New Yorkers would recognize this kind of action as they have been exposed to their own occupation following recent Manhattan bombings. Tanks, humvees and other kinds of military vehicles and equipment flooded the city, leaving behind shocking pictures of a city under siege..

Much was similar, though one difference between Manhattan and Charlotte was George Soros, who has made a habit of funding the provocations that the government then responds to. He obviously had a hand in the Charlotte riots that were precipitated by Soros-assisted Black Lives Matter.

Back in June, we covered Wikileaks exposure of the elite’s pre-planned “summer of chaos” when whistleblowers provided numerous documents illuminating Soros’ role with dedicated agitation from BLM.

Remember Deray Mckesson? He was the former BLM leader who had two of his email accounts hacked revealing that the Soros-backed social justice group was working with the Obama regime. The idea, he suggested, was to create so much chaos that martial law could be declared and elections canceled.

According to financial records and key players in the Ferguson Missouri protests, billionaire Soros donated $33 million to community organizers and organizations who helped turn the events there from a local protest into a politicized and televised race “crisis”.

Now there’s further evidence of George the puppet master along with his “open-borders” foundation, have been facilitating unrest.

Charlotte, North Carolina, is merely the latest riot-destination for his paid protesters, but one that comes with compelling evidence of his involvement.

About 70% of the rioters arrested had out of state IDs. No doubt they traveled to Charlotte in buses paid for by Soros.

In a CNN interview. Todd Walther, the spokesman for the Charlotte-Mecklenburg Fraternal Order of Police, told Erin Burnett, “This is not Charlotte that’s out here. These are outside entities that are coming in and causing these problems. These are not protestors, these are criminals.”

Yes, criminals – funded by a criminal. The most ridiculous aspect of these “peaceful protests” as CNN and MSNBC continue to call them, is that they are not protests. They are riots.

The rioting is obvious. “Protesters” broke into the Charlotte Hornets’ team store to steal basketball merchandise. “Protesters” looted the NASCAR Hall of Fame. “Protesters” vandalized and destroyed buses, stores and homes in poor black neighborhoods.

That’s probably how Soros lured them. He let it be known that looting would be the main “protest” in Charlotte.

When it comes to globalism and globalists, we don’t rule anything out. To the elites behind all of this – and Soros is just an employee – this is all a sick game. They actually enjoy controlling the sheeple and then laughing at their inability to recognize who’s manipulating them.

This is not going away with the end of the Jubilee Year in October or even with the end of 2016. It’s just getting started – and the false flags are growing more numerous. They feed the growing militarization around the country.

After the false flag shooting that occurred in Dallas, for instance, where the assailant was supposedly bombed by a drone before any information could be extracted from him, the NYPD was compelled to purchased $7.5 million worth of military grade protection equipment and weapons for themselves.

The NYPD officer from what Bloomberg called “the world’s 7th largest army,” even took pride in his force’s purchasing of these weapons and armor, saying, “There’s not a police department in America that is spending as much money or as much thought and interest on this issue of officer safety.”

Just what kinds of scenarios are these officers envisioning? If it weren’t for the camouflage it would be nearly impossible to differentiate between them and the actual military.

None of this seems to matter to Americans who don’t even bat an eye at these “troops” on their streets. Many, dumbed down by the fluoride in the water and in government schools, and propagandized by the mainstream media television programming, actually cheer when they see their very own forces of occupation.

Most of them are unaware of the existence of Posse Comitatus – the part of their constitution that used to prohibit troops on their streets in times of peace – let alone it’s nullification back in 2006, which made declaring martial law even easier in the event of a “terrorist attack” or “natural disaster”.

Americans are too busy watching sitcoms and fake news to figure out the disaster headed in their direction. And the ones that do figure it out are supposed to be discouraged by people like Soros.

That’s why there are so many news reports featuring Soros. And that’s why he’s never been arrested, by the way.

They want you to understand all the bad things he’s doing. And they want you to be clear on one thing: He can keep on doing it with impunity. No one is going to stop him. He’s going to continue his agitations until chaos rises up around the world.

The elites behind this world-shaping gambit want you to be thoroughly discouraged. They want to emotionally paralyze you.

There is violence and strife looming and it’s all being planned to control you. The elites intend to steal your wealth and livelihood by any means necessary. Stay one step ahead of them by getting your money out the financial system while you still can. To help your family and yourself survive and prosper through the collapse of the dollar, check out my book Shemitah Trends on Amazon or become a subscriber and receive the book free here.

We are now exactly one week from the end of the Jubilee year. Will something else happen before or on that date? Perhaps not. But, as we’ve described all year, all the pieces for continued chaos have been put in place.

And it won’t stop after October 2nd either. In fact, it looks like it is just getting started.

“Alarm bells have been ringing over the explosion of corporate debt levels in emerging economies, which now exceed $25 trillion … Damaging deflationary spirals cannot be ruled out”.

The writer’s name is Ambrose Evans-Pritchard and he’s one of Britain’s most prominent journalists, known for his hard-hitting reporting. He’s also the editor of the International Business section of the Daily Telegraph.

Here’s how it begins:

The third leg of the world’s intractable depression is yet to come. If trade economists at the United Nations are right, the next traumatic episode may entail the greatest debt jubilee in history. It may also prove to be the definitive crisis of globalized capitalism, the demise of the liberal free-market orthodoxies promoted for almost forty years by the Bretton Woods institutions, the OECD, and the Davos fraternity.

Alarm bells have been ringing over the explosion of corporate debt levels in emerging economies, which now exceed $25 trillion. “Damaging deflationary spirals cannot be ruled out,” said the annual report of the UN Conference on Trade and Development (UNCTAD).

Notice the phrase, “greatest debt jubilee in history.”

If you’ve been reading our blogs and publications, you know that for two years now , I’ve been writing about Shemitah Trends and the the Jubilee Year 2016. That’s no accident. I long ago discovered that the world’s elite organizers like to utilize both of these celebratory timelines to trigger catastrophic economic, sociopolitical and military events. Is it a game to them, or a kind of sly messaging? I don’t know, but we can see them doing it again in this article.

Right up front, Evans-Pritchard mentions a global “debt jubilee” and no one mentions that by accident. We’ve written in the past (see the article here in January) about how the BIS’s top economist William White used the phrase – and the writer who quoted him was none other than Ambrose Evans-Pritchard.

White claimed the world’s overall indebtedness was such that only a global forgiveness of debts would suffice to correct global finances. And here, once more, is Evans-Pritchard raising the decibel level to four or five alarms.

Maybe we should simply discount his reporting. But that’s probably not such a good idea. He’s a very important reporter whose father was an agent of British Intelligence. An article like this isn’t simply dashed off quickly. It has the ring of a declaration.

Here is the article’s summary sentence, toward the bottom:

What is clear is that world will soon need a massive and coordinated spending push by governments to create demand and bring the broken global system back into equilibrium. UNCTAD is entirely right about that.

What UNCTAD is calling for is the exact opposite of a free-market solution. We’re told that UNCTAD has stated what its execs believe to be obvious: Monetary policy is not working around the world. A “global new deal” is necessary, one to be directed by governments in concert probably with the UN itself.

Of course this program won’t work either, but it shoves the world a good ways toward global government, which is the desired goal.

This article may be bylined with Pritchard’s name but it is announcing the New World Order strategy going forward. Elites managing these programs intend to buy off the developing world with trillions of dollars of capital infusions. And they intend, it would seem, to alleviate the debt of the developed world via Jubilee.

This is how world government may be established, via directed bribery and money printing, not just intimidation and prison camps.

Pay attention to this article and to Evans-Pritchard. Writing this kind of article is his secret job. When there’s something especially important to be said, his pen is usually tapped.

We noticed this mouthpiece aspect recently when he wrote (here) what was for all intents and purposes a press release for a new central bank cryptocurrency, RSCoin, At the time, I wrote about Evans-Pritchard, saying, “The article is horrible central bank happy-talk that reads like the Bank of England wrote it for him.”

There’s no doubt this latest article is part of something bigger. “They” are preparing to move. Just last week, Barack Obama gave a speech at the UN where he said, “Sometimes I’m criticized in my own country for professing a belief in international norms and multilateral institutions. But I am convinced that in the long run,giving up some freedom of action — not giving up our ability to protect ourselves or pursue our core interests, but binding ourselves to international rules over the long term — enhances our security.”

In other words, he believes the US should give up freedom under the UN.

These statements are part of a long line of similar sentiments. George H.W. Bush, in 1991, was even more blatant, saying:

“We have before us the opportunity to forge for ourselves and for future generations aNew World Order, a world where the rule of law, not the rule of the jungle, governs the conduct of nations. When we are successful, and we Will be, we have a real chance at this New World Order, an order in which a credible United Nations can use its “peacekeeping” role to fulfill the promise and Vision of the U.N.’s founders.”

And, in 2003, David Rockefeller admitted full guilt in his role:

“Some even believe we arepart of a Secret Cabal working Against the best interests of the United States, characterizing my family and me as ‘internationalists’ and of conspiring with others around the world to build a more integrated Global political and economic structure – One World, if you will. If that is the charge, I stand guilty, and I am proud of it.”

And now Pritchard, the only “mainstream” reporter we know of who is mentioning the Jubilee, is warning of total collapse. This is the classic elite modus operandi.

Globalists love using mouthpieces like Pritchard to put the truth out in plain sight so after they have pull off their desired atrocities, they can point and laugh at the stupid plebs who had the truth right in front of their eyes all along. It also serves as a form of predictive programming, so when what they warn of what’s to come, people are more easily accepting of it.

The Elites increased transparency regarding their intentions is a clear sign to take action to conserve your wealth. Even a comprehensive reflation and jubilee won’t replenish your personal wealth. Chances are the handouts will be arbitrary and depend on your behavior and willingness to take orders.

Another article that demonstrates Pritchard’s association with the financial elites was published back on March 27th and was headlined, “Why America is Turning to an Englishman for Answers”.

Pritchard goes on to brag that he was the one who “”triggered a wave of disclosures” against former president Bill Clinton in addition to coordinating leaks and rumors that have thrown the financial markets into turmoil.

In fact, spies were and are regularly expelled from their host countries for doing the things Ambrose talked about, some even serve prison sentences. Nonetheless, Pritchard’s bosses at the Sunday Telegraph seem blissfully ignorant of these espionage laws.

This is no coincidence. A guy like this mentioning the Jubilee is a clear sign that he is simply a tool used to move markets and create chaos – just one of many puppets that has immunity.

The Elites increased transparency regarding their intentions is a clear sign to take action to conserve your wealth. This collapse is going to be so bad that those who lose the least will be the best off.

Lucky for us, our TDV portfolio hasn’t lost much, in fact it’s up a collective 200% this year and contains stock picks and options up over 1000% in some cases. Most people will never see returns like that by listening to CNBC or government registered financial advisors. Join us to protect your and your family’s assets in these risky times click here for more info

You can subscribe here to receive the most updated and pertinent investment information from the fastest growing financial newsletter in the world. When you become a member you will gain access to a wealth of information that will show you the right moves to make if you want to survive and prosper through the planned collapse of the financial and monetary system.

No one else has covered this agenda better than TDV and has profited from its advanced foreknowledge.

As we near the end of the Jubilee year and all plans have now been put in place for the NWO and the destruction of the West, this book, I hope, will serve to show people how it has all been planned for decades.

That book is also free to subscribers with a subscription to The Dollar Vigilante newsletter subscribe here

We are now less than two weeks from the official end of the Jubilee Year on October 2nd. We discuss much further in depth what we think will happen over the next few weeks in the newsletter.

But, already, all of the pieces are now in place for the NWO and planned collapse. Now it is just a matter of time until they set off massive military, political, financial, monetary and economic chaos to usher it in.

China has failed to curb excesses in its credit system and faces mounting risks of a full-blown banking crisis, according to early warning indicators released by the world’s top financial watchdog.

A key gauge of credit vulnerability is now three times over the danger threshold and has continued to deteriorate, despite pledges by Chinese premier Li Keqiang to wean the economy off debt-driven growth before it is too late.

The Bank for International Settlements warned in its quarterly report that China’s “credit to GDP gap” has reached 30.1, the highest to date and in a different league altogether from any other major country tracked by the institution. It is also significantly higher than the scores in East Asia’s speculative boom on 1997 or in the US subprime bubble before the Lehman crisis.

Studies of earlier banking crises around the world over the last sixty years suggest that any score above ten requires careful monitoring. The credit to GDP gap measures deviations from normal patterns within any one country and therefore strips out cultural differences.

It is based on work the US economist Hyman Minsky and has proved to be the best single gauge of banking risk, although the final denouement can often take longer than assumed. Indicators for what would happen to debt service costs if interest rates rose 250 basis points are also well over the safety line.

China’s total credit reached 255pc of GDP at the end of last year, a jump of 107 percentage points over eight years. This is an extremely high level for a developing economy and is still rising fast .

Outstanding loans have reached $28 trillion, as much as the commercial banking systems of the US and Japan combined. The scale is enough to threaten a worldwide shock if China ever loses control. Corporate debt alone has reached 171pc of GDP, and it is this that is keeping global regulators awake at night.

The BIS said there are ample reasons to worry about the health of world’s financial system. Zero interest rates and bond purchases by central banks have left markets acutely sensitive to the slightest shift in monetary policy, or even a hint of a shift.

“There has been a distinctly mixed feel to the recent rally – more stick than carrot, more push than pull,” said Claudio Borio, the BIS’s chief economist. “This explains the nagging question of whether market prices fully reflect the risks ahead.”

Bond yields in the major economies normally track the growth rate of nominal GDP, but they are now far lower. Roughly $10 trillion is trading at negative rates, and this has spread into corporate debt. This historical anomaly is underpinning richly-valued stock markets at time when profit growth has collapsed.

The risk is a violent spike in yields if the pattern should revert to norm, setting off a flight from global bourses. We have had a foretaste of this over recent days. The other grim possibility is that ultra-low yields are instead pricing in a slump in nominal GDP for years to come – effectively a trade depression – and that would be even worse for equities.

“It is becoming increasingly evident that central banks have been overburdened for far too long,” said Mr Borio.

The BIS said one troubling development is a breakdown in the relationship between interest rates and currencies in global markets, what it describes as a violation of the iron law of “covered interest parity”.

The concern is that banks are displaying a highly defensive reflex, and could pull back abruptly as they did during the Lehman crisis once they smell fear. “The banking sector may become an amplifier of shocks rather than an absorber of shocks,” said Hyun Song Shin, the BIS’s research chief.

This conflicts with what the Bank of England has been saying and suggests that recent assurances by Governor Mark Carney should be treated with caution.

Yet it is China that is emerging as the epicentre of risk. The International Monetary Fund warned in June that debt levels were alarming and “must be addressed immediately”, though it is far from clear how the authorities can extract themselves so late in the day.

The risks are well understood in Beijing. The state-owned People’s Daily published a front-page interview earlier this year from a “very authoritative person” warning that debt had been “growing like a tree in the air” and threatened to engulf China in a systemic financial crisis.

The mysterious figure – possibly President Xi Jinping – called for an assault on “zombie companies” and a halt to reflexive stimulus to keep the boom going every time growth slows. The article said it is time to accept that China cannot continue to “force economic growth by levering up” and that the country must take its punishment.

One bright spot is a repayment of foreign debt denominated in dollars. Cross-border bank credit to China has fallen by a third to $698bn since peaking in late 2014 as companies scramble to slash their liabilities before the US Federal Reserve raises rates. The tally for emerging markets as a whole has fallen by $137bn to $3.2 trillion.

China’s problem is internal credit. The risk is that a fresh spate of capital outflows will force the central bank to sell foreign exchange reserves to defend the yuan, automatically tightening monetary policy. In extremis, this could feed a vicious circle as credit woes set off further outflows.

The Chinese banking system is an arm of the Communist Party so any denouement will probably take the form of perpetual roll-overs, sapping the vitality of economy gradually.

The country was able to weather a banking crisis in the late 1990s but the circumstances were different. China was still in the boom phase of catch-up industrialisation and enjoying a demographic dividend.

Today it is no longer hyper-competitive and its work-force is shrinking, and time the scale is vastly greater.

…and BOE is also worried?

Bank of England concerned over rapidly growing Chinese debt bubble

Britain’s central bank has warned that growing Chinese debt is a threat to global financial stability. Chinese firms are borrowing faster than the GDP is growing, according to the bank. ….read further

The International Monetary Fund (IMF) has warned at the G20 summit in Hangzhou, China, that in the face of crises, the refusal to reform how things are functioning will lead to economic weakness in the global economy. “The latest data show subdued activity, less growth in trade and a very low inflation, suggesting an even weaker global economic growth this year,” the IMF told G20 leaders.

Indeed, we are looking at 2016 coming in as the fifth consecutive year in which global growth will be below the average of 3.7% which prevailed between 1990 and 2007. The IMF said: “Without strong political countermeasures the world could suffer a disappointing growth” for several years to come. Christine Lagarde told world leaders: “Even in the longer term the outlook remains disappointing.”

A number of people are asking if we are advising the IMF both in front of the curtain or behind. I have meet with former IMF board members as well as people pulling triggers in some central banks. But we have no arrangement to advise the IMF. If their forecasts are starting to reflect ours, it is curious, I admit. They may be looking at things using our lenses. But I have never met Lagarde and I do not advise the IMF. True, they may be looking at the Economic Confidence Model. Many countries do. There is no formal arrangement whatsoever.

As demands rise concerning social inequalities in many countries, this tends historically to only lead toward more regulation and protectionism. In the end, this is the expected knee-jerk reaction from politicians and in the end it only created a negative downward spiral to the detriment of free trade. The hunt for taxes and the sharing of all information to beginning among G20 members January 1st, 2017, will also lead to less investment. The EU decision to retroactively change the tax code of Ireland and the Apple deal, is a death-blow to the global economy.

Structural reforms are vital at this point to prevent a real economic depression on a global scale. In countries with still weak demand, the IMF is advocating monetary and fiscal policy should intervene more to promote growth. But bureaucrats are far too disconnected from the economy to ever manage things correctly. They historically attempt to force their will upon the markets and that has always resulted in disaster.

In regions where the monetary policy has been exhausted with negative interest rates having only a negative impact economically, only changes to the fiscal policy are even remotely possible to soften the hard landing we are headed into. The formula of simply creating temporary jobs with additional public investment building roads and bridges, are never sustainable and have never reversed the economic decline. On April 8th, 1935, Congress voted to approve the Works Progress Administration (WPA), a central part of President Franklin D. Roosevelt’s “New Deal.” The US share market rebound, but this was due to the dollar devaluation in 1934 following the bank holiday in 1933. The WPA kept hiring people reaching its peak in 1938 of over 3 million. The primary restriction was one person per family. Despite the claims, the WPA was a failure for there was no evidence whatsoever that it ended the Great Depression. It did provide relief and helped families make the transition from agriculture to skilled labor. So from the standpoint of retraining people, it did provide a foundation to build upon. However, such programs that fail to help people make such a transition within the work force are worthless in reversing an economic downtrend. In fact, if taxation is raised as a result, then it merely robs the right pocket to put some one in the left. That never provides economic growth no less stimulus.

The economic warning signs of a major slowdown in growth are appearing now on a global perspective from China and Japan to North American and Europe. The sharp decline in trade was reflected in the world’s seventh largest container shipping company Hanjin which declared bankruptcy in South Korea. Hanjin is the first prominent victim of the downturn in international maritime trade. There is little doubt that this is the canary in the coal mine providing a clear visible sign of a new economic Depression is looming on the horizon.

The sun is settling. It may appear to be rather beautiful. It is always the prettiest before nightfall.

…this of course is not only peculiar to the US, but across the entire world where the central banks are printing useless paper, or fiat money if you prefer.

Destroying our ability to discover the real cost of assets, credit and risk has not just crippled the markets–it’s crippled the entire economy.

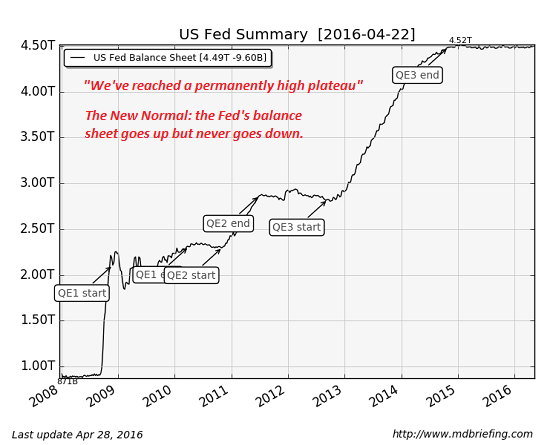

Is anyone else fed up with the Federal Reserve? To paraphrase Irving Fisher’s famous quote about the stock market just before it crashed in 1929, we’ve reached a permanently high plateau of Fed mismanagement, Fed worship and Fed failure.

The only legitimate role for a central bank is to provide emergency liquidity in financial panics to creditworthy borrowers. Once the bad debt (credit extended to failed enterprises and uncreditworthy borrowers) is written off, the system resets as asset valuations adjust to reality–how ever unpleasant that might be for the credulous participants who believed the ever-present permanently high plateau shuck and jive.

Just to state the obvious: Fed policies are not just insane, they’re destructive:

— Bringing future sales/demand forward by lowering interest rates to zero just digs a gigantic hole in future sales/demand. Funny thing, the future eventually becomes the present, and instead of a brief recession of low demand we get an extended recession of weak demand and over-indebted households and enterprises.

— Enabling massive systemic speculation by those closest to the Fed’s money spigot is insane and destructive, as capital is no longer allocated on productive returns and risk but on the speculative gains to be reaped with the Fed’s free money for financiers

— Buying assets to artificially prop up markets completely distorts the markets’ ability to price assets based on real returns and real risk.

Manipulating interest rates creates a hall of mirrors economy in which nobody can possibly discover the real price and risk of borrowing money. What would mortgage rates be without the Fed and the federal housing agencies (Freddie and Fannie Mac and the FHA) pumping trillions of dollars of federally backed mortgages into the housing market?

Nobody knows, because the mortgage market in America has been effectively taken over by the central bank and state.

The Fed’s entire policy boils down to obscuring the real price of assets, credit and risk with a tsunami of debt. The Fed’s “solution” to the economy’s structural ills is: don’t worry about risk, valuation or costs–just borrow more money for whatever you want: new houses, vehicles, stock buy-backs, Brazilian bonds, worthless college degrees, it doesn’t matter: there’s plenty of credit for everything.

The only thing that matters is your proximity to the Fed money spigot. If you’re a poor student, you get a high-cost student loan from the Fed’s flood of credit. If you’re a corporation or fiancier, well, the sky’s the limit: how many billions do you want to borrow or skim for stock buybacks or speculative carry trades?

The Fed’s control of the machinery of obfuscating price and risk has made us all members of the Keynesian Cargo Cult. Now we all dance around the Fed’s idols, beseeching the Fed the save us from our financial sins. We study the tea leaves of the Fed’s announcements, and hold our breath lest the worst happen–gasp–the Fed might push interest rates up a quarter of a percent.

This is of course totally insane.

Destroying our ability to discover the real cost of assets, credit and risk has not just crippled the markets–it’s crippled the entire economy. Wake up, America, and stop worshipping the false gods of the Fed. The sooner we smash the Fed’s idols and strip away their power to enrich the few at the expense of the many, the better off we’ll be.

My new book is #2 on Kindle short reads -> politics and social science: Why Our Status Quo Failed and Is Beyond Reform ($3.95 Kindle ebook, $8.95 print edition) For more, please visit the book’s website.

Global corruption costs trillions in bribes, lost growth … Public sector corruption siphons $1.5 trillion to $2 trillion annually from the global economy in bribes and costs far more in stunted economic growth, lost tax revenues and sustained poverty, the International Monetary Fund said on Wednesday. – Reuters

The IMF has just announced that doing away with corruption worldwide is “critical for the achievement of macroeconomic stability.”

The Reuters article informs us that this is “one of the institution’s core mandates.”

Our perspective is far different.

From what we can tell, the IMF and the World Bank act as a kind of macroeconomic tag team, enticing third world countries with massive loans and then ripping apart whole economies when the loans aren’t paid back on time.

We arrived at these insights in part due to John Perkins’ famous book, Confessions of an Economic Hit Man.

Here’s how TruthOut described the book during a 2014 interview with Perkins:

John Perkins is no stranger to making confessions. His well-known book, Confessions of an Economic Hit Man, revealed how international organizations such as the International Monetary Fund (IMF) and the World Bank, while publicly professing to “save” suffering countries and economies, instead pull a bait-and-switch on their governments: promising startling growth, gleaming new infrastructure projects and a future of economic prosperity – all of which would occur if those countries borrow huge loans from those organizations.

Far from achieving runaway economic growth and success, however, these countries instead fall victim to a crippling and unsustainable debt burden.

Reuters is reporting on a different and much more positive and responsible IMF. It’s portraying an IMF that is devoted to fighting corruption in order to benefit citizens around the world.

According to Reuters, “The Fund argues that strategies to fight corruption require transparency, a clear legal framework, a credible threat of prosecution and a strong drive to deregulate economies.”

But here, from The Daily Mail, posted in early April:

The IMF officials said a threat of an imminent financial catastrophe was needed to help reach a ‘decision point’, convincing German chancellor Angela Merkel on debt relief and Greece into accepting IMF “measures” against pensions and working conditions, said the transcript.

In other words, only a month or so ago, IMF officials were discussing a way to fake “financial catastrophe” to move Greek negotiations along.

Is that part of the “transparency” that the IMF seeks? Here’s what Perkins told TruthOut about Greece:

I want to draw upon Greece’s history. You’re a proud, strong country, a country of warriors … I would encourage the people of Greece to stand up: Don’t pay off those debts; have your own referendums; refuse to pay them off; go to the streets and strike. And so, I would encourage the Greek people to continue to do this.

… Don’t accept this criticism that it’s your fault, you’re to blame, you’ve got to suffer austerity, austerity, austerity. That only works for the rich people; it does not work for the average person or the middle class.

Build up that middle class; bring employment back; bring disposable income back to the average citizen of Greece. Fight for that; make it happen; stand up for your rights; respect your history as fighters and leaders in democracy, and show the world!

Perkins is exhorting Greeks to confront the IMF and the EU when it comes to the “austerity” that has been inflicted on the country.

Seen from Perkins’s standpoint, the problems affecting Greece are predictable enough. The country couldn’t pay back its sovereign debt in a timely manner and now Greeks have lost savings, pensions and whole bank accounts.

But Reuters is not writing about the IMF that Perkins is portraying.

The IMF paper – as Reuters reports it – doesn’t deal with any of these troubling issues. The crux graf of the Reuters’ article is this one:

[The IMF] said corruption’s indirect costs are substantially higher, reducing government revenues by encouraging tax evasion and reducing incentives to pay taxes, leaving less money available for public investments in infrastructure, health care and education.

We just wrote about this the other day. On what planet do international bureaucrats find that government revenues are in any sense appropriately or efficiently delivered?

Services provided by the -European Union are so lamentable that up to half of the countries now in the EU want to have referendums on leaving.

In the US huge amounts of tax revenue goes to the military-industrial complex, which in turn is fighting a “war” against terrorism. But if one uses available, public reports on the Internet, it soon becomes clear that war is a phony one and the terrorists have actually been put in place by US facilities.

Once more, the IMF seems to have a different grasp of reality regarding taxes and the way governments function.

More from Lagarde:

“Corruption also has a broader corrosive impact on society. It undermines trust in government and erodes the ethical standards of private citizens,”

And here is the real reason for this sudden attack on global corruption:

Lagarde is due to participate in a British government-sponsored anti-corruption summit in London on Thursday that will include U.S. Secretary of State John Kerry and other senior officials including the presidents of Nigeria and Afghanistan.

We can see that the global regime we’ve covered previously is being put into place. First came the Panama Papers and now a more general attack on “corruption.”

Conclusion: This is part of an international power grab. The IMF and other agencies controlled by the West, and by the US and Britain in particular, are being repositioned as more aggressive, international regulators. Will this fight against international corruption yield positive results? Not really. It will simply endow obviously corrupt entities like the IMF and World Bank with even more power … and thus enhance the misery they already inflict.

For years, those who face the costs of educating themselves or their children hear a nearly incessant drum beat of how expensive a college education is, and how much debt they’ll likely be taking on. On the other hand, we’re told repeatedly that a college education is absolutely essential because people with a college degree allegedly make a million dollars per year more than those who do not attend college.

Most everyone agrees that tuition and fees are certainly increasing in terms of the price tag. There is far less agreement, however, on why the price of a college education is going up so quickly.

The answer lies in a mixture of government policy and the fact that colleges and universities today spend vast amounts of money on amenities and staff that have little to do with classroom instruction. Moreover, the tastes of many consumers of education have changed toward the more opulent, and many aspects of the so-called “college experience” which were virtually non-existent 30 or 40 years ago, are today considered to be necessities for college students.

And finally, many students spend vast amounts of money on college degrees that will never contribute much to actually paying off loans or contributing much toward the graduates’ actually earning a living.

Government Subsidies Enable Price Increases

One of the more basic observations of economists of all types is the fact that less of a good or service is demanded the higher the price goes. This is why the demand curve is downward sloping, and why fewer people will want ten-dollar hot dogs than will want two-dollar hot dogs, all else remaining equal.

On the other hand, if the government gives out grants and loans for buying hot dogs, or if people are hoodwinked into believing they’ll make a lot more money if they only eat more hot dogs, the price will rise quickly.

There is no doubt that overall demand for a college education has increased based on the idea that a college education is the key to wealth. The broad conclusion that a college education greatly increases one’s earning potential greatly over one’s lifetime ignores the fact that not all college degrees are created equal.

As this data shows, only certain college degrees are likely to bring back a good return on the investment. While economics and engineering majors are likely to pay off loans quickly and maintain employment over the long haul, people who spent six figures at a fancy university to get a degree in sociology of Latino studies are likely to struggle to pay off their debts.

Moreover, if you’re one of those people with a humanities degree, your electrician and your mechanic are often likely to make more money than you. And, they gained that higher earning capability after spending far, far less in terms of time and money on their education. Once we begin to look at things on a case-by-case basis, the advantages of a college degree can melt away.

So, much of the increase in demand for a college education is based on a false premise: the idea that any college degree with get you a living wage. What you study remains very important.

Nevertheless, going to college has for centuries been seen as a way to gain or maintain financial success, and the idea did not just enter the minds of the general population in the last thirty years, when tuition prices began to skyrocket.

What changed was the increased presence of student loans, and especially loans at low interest rates, thanks to government guarantees and loose monetary policy.

Last year, University of Colorado law professor Paul Campos, who is hardly an advocate of laissez-faire, attacked the claim that direct government funding of colleges is being cut, while also noting the role of student loans in increasing costs of college:

The conventional wisdom was reflected in a recent National Public Radio series on the cost of college. “So it’s not that colleges are spending more money to educate students,” Sandy Baum of the Urban Institute told NPR. “It’s that they have to get that money from someplace to replace their lost state funding — and that’s from tuition and fees from students and families.”

In fact, public investment in higher education in America is vastly larger today, in inflation-adjusted dollars, than it was during the supposed golden age of public funding in the 1960s. Such spending has increased at a much faster rate than government spending in general. For example, the military’s budget is about 1.8 times higher today than it was in 1960, while legislative appropriations to higher education are more than 10 times higher.

In other words, far from being caused by funding cuts, the astonishing rise in college tuition correlates closely with a huge increase in public subsidies for higher education. If over the past three decades car prices had gone up as fast as tuition, the average new car would cost more than $80,000.

The data can only show a correlation, but basic economic theory shows us the causation. The government subsidies to students have lowered the perceived cost of attending college. This, in turn, allows a larger number of students to pay the ever-increasing tuition bills. Put another way, the elasticity of demand for a college education has increased significantly thanks to the fact that students can now just go get a low-interest unsecured student loan rather than have to save the money to use a high-interest private-sector loan.

Without these loans, students would be far more sensitive to increases in the cost of education, and colleges would have to find ways to cut costs in order to remain competitive in terms of pricing. With a nearly endless stream of government loans, however, colleges need never have to worry about cutting costs. Government subsidies will simply make up the difference, and price-sensitive students will go to college anyway. The downside comes later when students must then pay off large loans.

Increases in Cost Don’t Go to Classroom Instruction

Campos also points to the fact that we can’t blame the price increases on the cost of instruction going up. The amount of resources being devoted to actual classroom instruction, Compos notes, has changed little in terms of real dollars. What has changed is the cost of administration at colleges, where

a major factor driving increasing costs is the constant expansion of university administration. According to the Department of Education data, administrative positions at colleges and universities grew by 60 percent between 1993 and 2009, which Bloomberg reported was 10 times the rate of growth of tenured faculty positions.

Even more strikingly, an analysis by a professor at California Polytechnic University, Pomona, found that, while the total number of full-time faculty members in the C.S.U. system grew from 11,614 to 12,019 between 1975 and 2008, the total number of administrators grew from 3,800 to 12,183 — a 221 percent increase.

And administration isn’t the only place in which colleges are pouring money. Students are also paying for lavish amenities such as recreation centers and luxurious dorms where each room has its own bathroom, and much more.

In their defense, college administrators have trotted out the usual old saw that “budget cuts,” and not a country-club living standard on campus, is to blame for increasing tuition and fees for college students, but the immense increases in college fees that are necessary to support these new amenities would never be economically viable if it weren’t for easy access to cheap student loans.

Many People Make Purchases Based on Branding, Not Education Quality

Another factor behind rising costs for some students is the fact that students purchase costly programs not necessarily for the education they provide, but for the status of having attended a prestigious name-brand college. Just as people will spend hundreds or thousands more on a handbag or automobile for the purposes of conspicuous consumption, many students will do the same with their college educations, believing it will raise their social status.

Yet again, we find that what you study matters more than where you do it. So, it is entirely plausible that the student who studies accounting at the thoroughly unglamorous public university known as IUPUI in Indianapolis is likely to earn more than a psychology major at some elite East Coast university.

And, of course, one makes a logical error by assuming that successful Harvard graduates were successful because of their attendance at an elite university. People who get into Harvard are already highly driven over-achievers. Harvard students aren’t slackers who are molded into elite intellectuals and workers due to the amazing quality of instruction at Harvard. That’s not how it works.

This isn’t to say there’s something “wrong” with choosing to attend an elite college if the opportunity presents itself. Consumers make decisions based on a variety of subjective criteria, and it may be that for some of them, consuming the product known as “Ivy League college” is very important and well-worth the additional cost.

However, these people tell us little about the true cost of obtaining an education. Those who choose to attend costly elite colleges — when opportunities exist for attending more modestly priced programs — should be excluded from analyses that claim to tell us how expensive education has become for the average person.

Many People Are Willing to Pay Extra for the “College Experience”

Finally, it’s important to note that much of what drives demand for colleges, especially among the middle and upper classes, is a desire to get the so-called “college experience” which has nothing to do with the quality of instruction or one’s future earning potential.

In truth, living on campus as a college freshman, and taking advantage of all the entertainment, lifestyle, and social amenities offered to live-in students, is a luxury that is not essential to obtaining an education. Students who live off campus, of course, often report feeling “left out” or at a disadvantage in terms of finding the right social events.

These things are not without value, and many students may conclude for themselves that the “college experience” is worth the extra cost, but let’s not pretend that such experiences are essential to obtaining a college education.

Moreover, simply attending a costly four-year college in one’s freshman year is an unnecessary luxury overall, regardless of where one lives. As billionaire Mark Cuban — an Indiana-University grad — correctly notes in this video, from a financial point of view, it makes far more sense to attend one’s freshman and sophomore years at the least expensive college one can find where college credits will transfer up to more costly four-year schools.

These economic facts won’t stop many students, however, from insisting that they absolutely must attend an expensive liberal arts college in order to get the full college experience. (This woman just had to go to NYU and took out $100,000 in loans to get a degree in religious and women’s studies.)

The Cost of Education vs. the Cost of “College”

As with any consumer’s preference for attending an elite school, we cannot say that any particular student is wrong for attending a school that costs $25,000 in tuition per semester. It may be perfectly rational, from the student’s point of view, to attend a college because it has pretty buildings or the students are good-looking.

Being surrounded by beautiful people and beautiful buildings really is something of value. However, let’s not pretend that those amenities are essential to the process of obtaining an education or increasing one’s earning potential.

In the background of every political discussion over higher education is the assumption that a college education is essential to combating poverty and other social ills. So, if we’re going to engage in an honest discussion of the true cost of an education, we have to differentiate between what is being paid toward financial betterment, and what is being paid by some people toward a four-to-six-year vacation.

What a Free Market in Colleges Might Look Like

Student loan subsidies have so distorted the market for higher education that we can’t even tell the difference anymore. In a world of more market-oriented colleges, we’d be seeing colleges that work strenuously to reduce costs while increasing the quality of faculty instruction. Instead, what we find is a race to produce ever more luxurious amenities or funnel more and more money to six-figure-salaried administrators and staff to run a high-end rec center for students.

Colleges would focus on providing easy-to-attend classes for part-time workers (many of whom are low-income) who must attend college at the lowest cost possible. Students would focus on fulfilling basic requirements at lower cost schools and community colleges while waiting to access more costly lab facilities and other resources in the junior and senior years. (Many low-income students already do these things, but in the absence of subsidized loans, the total numbers using these strategies would be far greater.)

Certainly, those with the means would still attend costly luxurious schools, but most would recognize that those students are paying for something other than education. Far larger numbers of students, though, would attend colleges that specialize in delivering an education in a timely and cost-effective manner with few frills. The number of students attending amenity-laden schools would fall considerably, and many small liberal arts colleges would go out of business. Urban and suburban campuses, while less “sexy,” would benefit instead as students turned toward more economical easy-to-access colleges that are more focused on job skills and integrating students into the larger community that includes employers and industries that need employees.

As long as government student loans remain a dominant factor in the pricing of higher education, though, we’ll continue to see more and more growth in the cost of higher education which will continue to be a boon for the colleges themselves, while placing a heavy burden on students who don’t understand how little of what they pay actually goes to education.

I think the Boomland scenario is in most cities of the world and especially so here in Kuala Lumpur. Construction is everywhere and these so called “developments” have become a hazard for the city folks. Don’t they know what’s going on in the decrepit financial system? Yes and no. But, ‘the show must go on’ ….as they say. I guess we’ll just wait for the bubble to burst.

We want this time to be different so badly, we can almost taste it.

.

If you visit San Francisco, you will find it difficult to walk more than a few blocks in central S.F. without encountering a major construction project. It seems that every decrepit low-rise building in the city has been razed and is being replaced with a gleaming new residential tower.

Parking lots have been ripped up and are now sprouting condos and luxury rental flats.

The influx of mobile/software tech into the S.F. Bay Area has triggered not just a boom in tech but in all the service sectors that cater to well-paid techies. This mass of new people has created traffic jams that last virtually all day and evening, and overloaded the area’s BART transit rail system such that trains at 11 pm are as jammed as any during rush hour.

This phenomenal building boom is truly something to behold, as it has spread from S.F. to the East Bay as workers priced out of S.F. move east across the Bay, driving up rents to near-S.F. levels.

.

This is of course a modern analog of the Gold Rush in the 1850s, and the previous tech/building boom in the late 1990s: an enormous influx of income drives a building boom and a mass influx of treasure-seekers, entrepreneurs, dreamers and those hoping to land a good-paying job in Boomland.

.

The same phenomenon has been visible in the Oil Patch states every time oil/gas skyrocket in price.

.

We know how every boom ends–in an equally violent bust. Yet in the euphoria of the boom, it’s easy to think this one will last longer than the others.

.

I distinctly recall the mass excitement of COMDEX in 1999, the big computer-tech trade show in Las Vegas. The city was packed, the convention centers were packed, and an enormous banner announcing the then revolutionary slogan “the network is the computer–Sun Microsystems” welcomed the faithful.

.

I saw Bluetooth demonstrated for the first time in that show (at a Motorola booth), and dozens of other consumer technologies that never quite caught on–kits to turn your PC into a TV, etc.

.

A year later the bubble had burst, and a decade later Sun Micro had lost its edge and would end its glorious run in the ignominy of being sold to Oracle for pennies on the dollar.

Across the Bay in Oakland, new relatively large 1-bedroom flats with Bay views are asking $3,300 a month. The same flat in S.F. would fetch $4,000 or more per month. Techies working for free on a buddy’s start-up have famously rented the space beside the washing machine in a laundry room for $400 a month.

.

How many average workers can afford to pay $40,000 a year in rent? After taxes, even techies earning $80,000/year would have little to show for their labor once they paid $40K after $20K in taxes and deductions have been subtracted from their annual wage.

.

The current Gold Rush will collapse, and as the newly fired marginalized workers pack up and leave, nobody will be renting the flats for $4,000/month. The owners will try reducing the rents to $3,000/month, and with no takers, they will go bust and the gleaming towers will be auctioned off. Eventually rents will decline to what people can actually afford.

This process will take a few years, as owners are reluctant to accept secular declines in rent and the resulting insolvency. Restaurants and other secondary businesses that arose to serve the techies will hang on, paying insane rents, for a few months and then give up losing money and close.

.

We naturally cling to the euphoria and glory of a boom; they generate such hope and positive emotions. The bust is no fun at all, a slow cascade of layoffs, insolvencies, moves to cheaper and far less exciting locales, busted dreams and all the mourning that accompanies the shattering of dreams and hopes.

.

Knowing all this doesn’t prepare us for the bust, any more than the initial signs of a boom prepared us for the bubble. We want this time to be different so badly, we can almost taste it. But this time is only different on the margins; the flavor of the bust remains the taste of ashes.

Russian “Weaponized Default” Law Threatens Collapse Of Entire Western World

By: Sorcha Faal, and as reported to her Western Subscribers